Global Supply Chain: All Roads Lead to (and from) China

China’s emergence and entanglement with global supply chains

Over the past three decades, the Chinese Communist Party (“CCP”) has done a miraculous job of expanding its spheres of influence with context to global supply chains. The nation’s approach to securing critical raw materials abroad, investing in refining capacity and manufacturing at home, and leveraging vulnerabilities in the global supply chain strengthened China’s position while simultaneously building global reliance.

However, today we are facing renewed threats to the supply chain with more reported lockdowns from China. Despite the world being ready to finally move past the threat of COVID, since the beginning of the pandemic, China has implemented increasingly strict protocols to deal with rising caseloads. This has culminated in China’s current “Zero COVID” policy – with the aim of, unsurprisingly, keeping COVID case counts as close as possible to zero. As a result of this policy, slight upticks of COVID cases in China have led to lockdowns so strict in China that many Americans could not fathom here at home. Under China’s Zero COVID policy, affected residents of a town are required to stay indoors, with limited time frames at which they can venture out for food, medicine, and emergency medical treatments. Recently, Guangdong province - home to China (and arguably the world’s) manufacturing hub - has seen an uptick in cases and the corresponding Zero COVID lockdowns. The fallout, in turn, has been a shutdown of nearly all social and economic activity in the most important manufacturing hub in the world.1 So, what might this mean for the Chinese and global economy, and therefore investors?

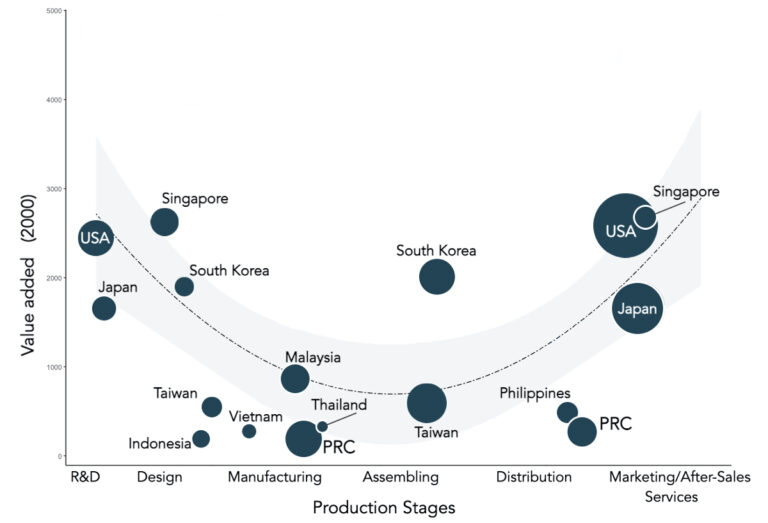

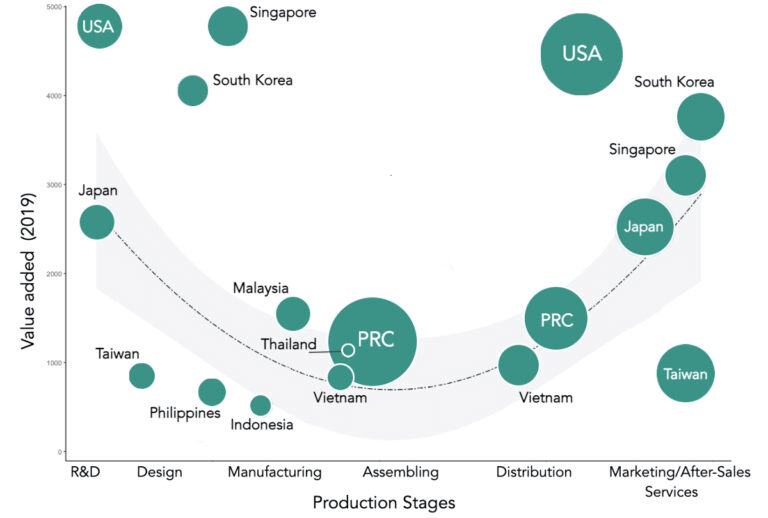

To better understand where China fits in the global context of supply chains, we find it helpful to see where the nation plots on the “Smile Curve” – a chart created by Stan Shih, the founder of the PC maker and technological manufacturing behemoth Acer, which represents the magnitude of a particular nation’s value-added services in each segment of the global value chain.

Positions Along Smile Curve See Little Change, 2000 vs. 2019

Source: Macro Polo

In relation to the other advanced economies, over the past couple of decades, China’s position along the curve has largely been stationary towards the bottom end of the curve, tilting towards manufacturing, assembling, and distribution. Why is this portion of the Smile Curve important? Well, for starters it indicates that China has gained unprecedented control of global supply chains and is a reason why most products you see around the globe are “made in China”. The control has since evolved in this new digital age, and is spreading further up both axes of the Smile Curve. Chinese companies have developed expertise in the higher value-added portions of the value chain. Technology and R&D, as well as marketing teams are reportedly making up a growing portion of Chinese businesses relative to the manufacturing labor workforce. The control in these crucial portions of the value chain is building a unique breed of companies out of the east, and in turn, likely increasing China’s control of the more advanced stages of the supply chain that had typically been dominated by more developed economies.

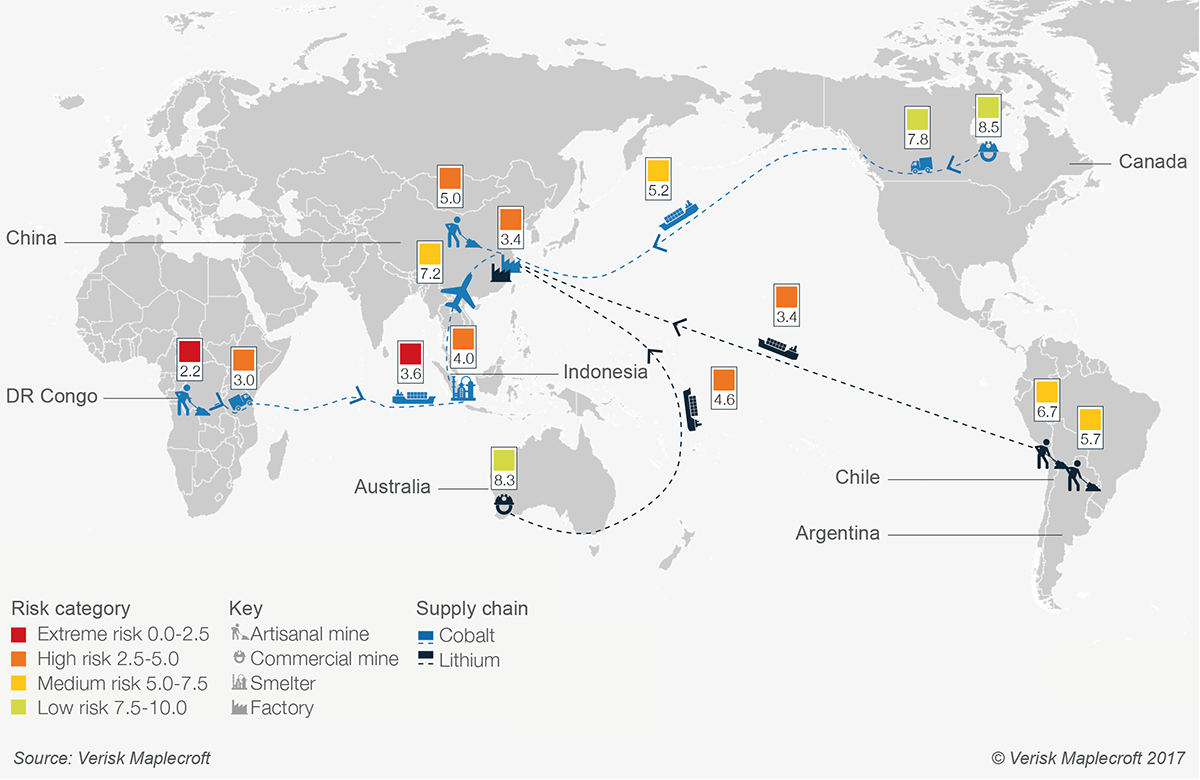

Pin-pointing risk across the lithium-ion battery supply chain

Source: Spend Matters - The Supply Chain Risks Lurking Behind the Electric Vehicle Boom

Rare Earths

There are many strategic commodities for which China has dominated the market, but one increasingly important commodity class with respect to new energy initiatives is rare earths. Like their name suggests, rare earths are materials found in the earth’s crust that are not in fact rare, but rather difficult to isolate, and serve as the backbone and engine to nearly all modern technology and power sources. They are of particular importance when weighed against the ambitions of China’s 14th Five-Year Plan, the Communist Party’s centrally managed plan for the nation’s economy. Perhaps analogous to the Build Back Better plan with respect to infrastructure/new energy initiatives, but with actual credence, because unlike our often messy democratic system, China is a nation-state built on central economic planning.2 Why this matters is largely due to rare earths being at the grassroots of this highly complex global supply chain. They are the building blocks for the many consumer electronics and complex consumer technology products that move our everyday lives. They are a strategic commodity that requires considerable expertise to utilize by transforming mined concentrates into refined oxides ready to help feed our global appetite for electronic goods.

The success of the CCP with regard to rare earth metals concentration traces back to the mid-1980s, when the government entered the nascent industry by means of issuing tax rebates to rare earth miners and refiners. These rebates in turn lowered costs for Chinese mining companies, allowing them to take away share from global competitors. As a result, China’s rare earth extraction reportedly ballooned ~6x and its market share jumped from 21.4% to ~60.1% in the proceeding decade. Today, China produces roughly 85% of the world’s rare earth oxides (fuel cells, ceramic bulletproof vests) and approximately 90% of rare-earth metals (lithium in batteries), alloys (radar, jet engines, spark plugs, telescope lenses), and permanent magnets (hard drives, speakers, maglev trains, and roller coasters).3

Lithium-ion batteries (one of many examples)

While there are many industry recipients throughout the global value chain in which these rare earth metals land, one that is front and center, and currently dominated by the CCP is the lithium-ion battery industry. With respect to where current battery technology stands today, that is, highly reliant on cathode materials such as lithium, nickel, manganese, and to a decreasing level, cobalt. China reportedly has the highest demand in the world with respect to battery materials – a function attributed to China having the highest density of battery manufacturing capacity globally. This sort of advantage on two highly critical portions of the supply chain (upstream and downstream) is outstanding, and in turn creates a competitive advantage for China as the world electrifies, and the use of electric vehicles & battery storage becomes ubiquitous.

The evolution of China’s integration into the global battery supply chain is another economic feat for the CCP. Much of the world’s lithium utilized in electric vehicles today has at some point worked its way through China, and that’s because approximately 80% of the world’s raw material refining and over 70% of the world’s battery cell capacity are located throughout the provinces of China.4 The ecosystem in China has created some impressive champions, with names such as CATL and BYD, the largest Chinese battery cell manufacturers, on the battery and vehicle side (downstream), and names such as Ganfeng and Tianqi on the mining side (upstream).

Interestingly, however, is that China struggles to compete on an international level with their domestic supply of rare earth elements. Part of their spheres of influence has led them to negotiate terms with dependent regions in Western Australia and South America for their lithium feedstock. The upstream players mentioned above formed strategic joint ventures with local players to operate mines in these regions, then ship material to China to be refined. In essence, the global supply chain here is rather complex. Often materials are mined thousands of miles away from refining sites in China. After refining, the materials are ready to use internally for battery products or redirected thousands of miles away to companies abroad.

Today, China is known as “the world’s factory”, and with good reason. The manufacturing ecosystem blossomed over the past few decades due to a variety of factors including an abundance of direct government subsidies, low (to no) labor costs, low taxes and duties, and a lack of regulatory restrictions. This environment, coupled with an incredible source of cheap domestic supplies of rare earths, allowed Chinese manufacturers the opportunity to scale up the production of essential products.

In January of 2022, China announced the merger of three leading rare earth companies and the creation of a new state-owned enterprise, called China Rare Earth Group, or as the Financial Times calls it, China’s “Aircraft Carrier”.5 Upon its announcement, many voiced their uneasiness about the deal throughout the international community. The new state-controlled behemoth will reportedly have power over 60–70% of Chinese rare earth production, which in turn translates to 30–40% of global supply.6

With respect to lithium-ion, the CCP is starting to see resistance and competition on a global scale, and this involves nickel refining - a key input to high energy density batteries used in modern electric vehicles (think Volkswagen & Tesla). Indonesia, a nascent player in the nickel refining ecosystem is starting to tilt the scale and overtake China as the top refined nickel producer.

Our recent history of COVID and geopolitical strife highlight the consequences of disruptions to products with a high market concentration. Not all too long ago, we saw the limitations of global supply chains when utilization rates of quintessential players hits near standstill. As we’ve said, supply chains are highly intertwined, and problems brought forth by the pandemic show just how disruptive reliance on individual firms, or nations, can be.

Across the globe, there are reports of emerging cross-national partnerships between governments, with ambitions of forging new alliances to take on the CCP. We are especially seeing this driven by many western countries and Asia Pacific nations.

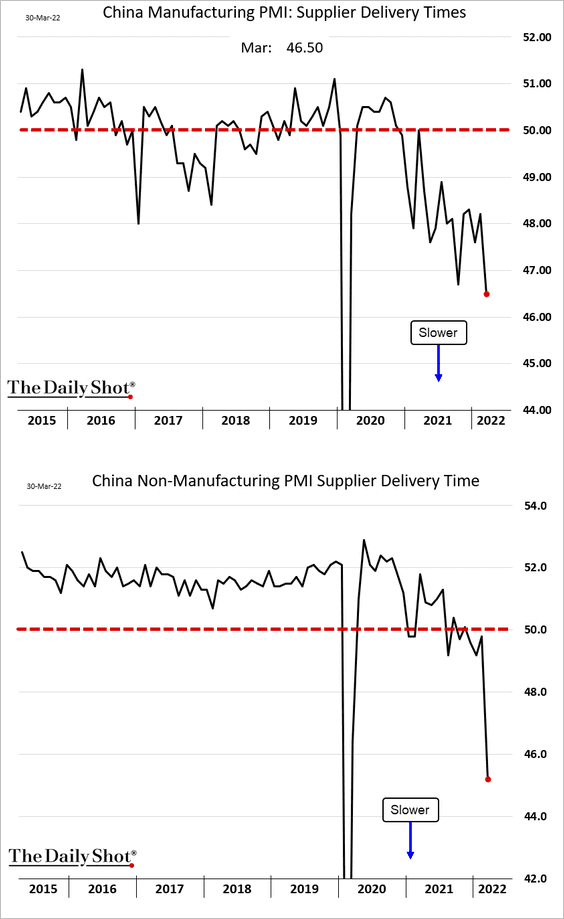

China Manufacturing and Non-Manufacturing PMI: Supplier Delivery Times

Source: The Daily Shot

While newly forged alliances likely hope to reclaim independence from the CCP, building the necessary infrastructure to support these ambitions doesn’t happen overnight. And unfortunately, recent news highlights the importance of moving away from this precarious system of offshoring, layered upon just-in-time production. Near the end of March, China began one of its most extensive COVID lockdowns in the past two years as part of the nation’s ongoing “Zero COVID” strategy – some restrictions more stringent than that seen in late 2019. The southern region of China, home to much of the nation’s manufacturing and financial hubs, has been on lockdown due to the recent outbreak. Though the effects on a global scale have not been felt, something to keep a key focus on is the manufacturing data coming out of China, which paints a fairly concerning picture.7

Moreover, as we recently discussed in our piece “China, Russia, and the West: A Game of Chess”, the global economy could see further threats coming out of China. The war in Ukraine has presented China with what is likely a zero-sum choice between a stronger geopolitical relationship with Russia and maintaining its economic ties with the West. As China’s rhetoric towards Taiwan, as well as disputed islands in the South China Sea, has escalated under Xi Jinping’s presidency, and its territorial ambitions have increased alongside the growth in its economic might, China appears to be inching closer to a more aggressive stance in its backyard. While so far, Russia’s failure to achieve its original goals in its war with Ukraine and the West’s forceful and unified response seem to have reduced the risk of an invasion of Taiwan, unifying the two Chinese states has been a core goal of the CCP since it established control of mainland China. China’s desire to capture and integrate Taiwan back into the Mainland is anathema to the West. A decision to invade will require support from allied nations like Russia, now a pariah to the developed world, and thus, any move on Taiwan can expect a similarly strong response from the West, likely in the form of economic sanctions. Therefore, China today faces a choice: closer ties with Russia, and the creation of a geopolitical alliance to rival the West and gives China the power to achieve its territorial ambitions, but at the cost of the economic relationships that have driven their phenomenal growth; or maintaining the status quo, with the world heavily integrated with the Chinese economy and keeping Russia at arm’s length, at the cost of foregoing or at least delaying control over Taiwan. As we have illustrated today, due to the world’s reliance on Chinese manufacturing, the global economy is quite sensitive to not just the economic but also the social and political actions that China takes. Whatever China’s ultimate intentions are with Taiwan will have ramifications for the markets, and an attempt to seize Taiwan will likely leave China politically and economically isolated and potentially exacerbate the geopolitical volatility we have seen of late, with potentially huge consequences for investors. With so many potential surprises, advisors and their clients have much to keep an eye on in Asia.

We believe investors may need to brace for yet more volatility based on recent global developments. As discussed in this Insight, China is an integral part of the world’s supply chain and their current Zero COVID policy may cause further disruption to the production of critical goods at home and abroad. Between the recent Russia conflict, and a potential new threat of further global supply chain tribulations, companies fighting tooth and nail to boost output and become profitable may struggle in this difficult global environment. For these companies, a rising interest rate environment brings potential hindrance to the future cash flows of their businesses. This ultimately could lead to a narrower path to profitability with the potential for shrinking gross margins, higher operating costs, and more expensive debt financing. As we’ve recently seen, supply and demand-side shocks have the potential to really derail things, particularly with a global economy dealing with the fallout of rate rises and Russian aggression in Ukraine.

Ultimately, active management strategies and, more specifically, alternative investment strategies have historically demonstrated an ability to reduce the overall risk to global macroeconomic disruptions on an investor’s portfolio. While there is no assurance of future results, a few potential areas of opportunity during turbulent market environments may include Relative Value, Distressed and Global Macro. Financial advisors, at the same time, are encouraged to evaluate the potential risks associated with hedge fund investment strategies.

Sources:

- Foreign Policy, March 2022. "Shenzhen Covid Lockdown"

- Fujian Government, August 2021. "China's 14th Five-Year Plan"

- CSIS, May 2021. "China Rare Earths"

- Energy Post, January 2022. " Critical Raw Materials for the Energy Transition"

- Financial Times, December 2021. "China Merges 3 Rare Earths Miners"

- East Asia Forum, March 2022. "China Rare Earth Consolidation a Cause for Concern"

- Fortune, March 2022. "Shenzhen Lockdown Supply Chain"

Learn more about the third-party global macro, relative value, and multi-strategy hedge funds on our platform and how your clients can allocate to these strategies.