Investing in Alternatives Continues to Gain Momentum: A Case Study on Pension Funds

Insight Highlights

- Pension funds are perhaps one of the biggest asset allocators and are required to meet their respective plans’ return targets so that their beneficiaries can retire comfortably.

- Endowments allocate 20 percentage points more to alternatives than pension funds on average. This difference of 20 percentage points is a big opportunity for pension funds to attempt to enhance their returns and help close the funding gap they face between their assets and their obligations.

- A study published by Ernst and Young in November 2020 found that alternative investments outperformed during the early days of the pandemic, helping to mitigate the big crash in stocks and bonds that could have made pension fund results look devastating.

Gain exposure to institutional private equity and hedge fund strategies that may minimize risk for your clients' portfolios.

In a low interest-rate environment and with government bonds offering paltry returns, pension funds can no longer look to government bonds for a sufficient return. Investing in alternatives such as private equity, hedge funds, infrastructure, and venture capital has the potential to offer a solution for pension funds.

At its Investor Day, the private equity behemoth KKR pointed out, “Pension funds, where we have a large presence today, 30% of their assets are in alternatives. Endowments it's over 50%. Individual investors it's less than 5%. We believe that number is going to go up over time.”

Percentage of Assets in Alternatives

This shows that pension funds have a 20-percentage points margin between their allocation to alternatives versus the same allocation by endowments. This difference of 20-percentage points is a big opportunity for these funds to attempt to enhance their returns and help close the funding gap they face between their assets and their obligations.

The much smaller individual-investor allocation is where astute RIAs and independent money managers may have a chance to add value for their clients. By investing in alternatives, money managers can find creative ways to avoid investing in low returning asset classes like government bonds, which lowers risk but also lowers long-term returns.

As US News points out, “investing in alternatives is not for everyone. Access is limited to high-net-worth individuals and entities who are allowed to invest in securities that are not always registered with financial regulators. These investors usually fall into two groups: accredited investors and qualified purchasers.” Nevertheless, as pension allocation to alternatives show, more interest is turning towards investing in alternatives as momentum continues to build for the asset class.

Investing in Alternatives Has Made Pension Funds Safer

According to a recent article published in Bloomberg, there is overwhelming evidence that moving away from stocks and bonds and investing in alternatives has made public and private retirement plans less risky.

Most institutional portfolios have increased their alternative investments from around 5% or less in 2000 to 30% or more. The result has been to lower risk dramatically that helped to increase returns. And the 2021 annual reports from pension funds should show a continued move towards investing in alternatives.

A study published by Ernst and Young in November 2020 found that alternative investments outperformed during the early days of the pandemic, helping to mitigate the big crash in stocks and bonds that could have made pension fund results look devastating:

Alternative managers outperformed their performance expectations during COVID-19, especially in private equity, where a ratio of 4:1 felt their managers outperformed expectations. Hedge fund performance varied by strategy, but on average almost all significantly exceeded major benchmarks. When major indices were down 15%–20% in early 2020, many hedge funds were only down low single digits. Funds demonstrated their value in preserving capital in the downturn while opportunistically stepping in to capitalize on market dislocations. (Bloomberg, May 2021)

According to Aaron Brown, who is a former managing director and head of financial market research at AQR Capital Management, Pennsylvania teachers and most public pension fund beneficiaries can look forward to generally good news in 2021. The long-term problems — overpromising and underfunding — haven’t changed but modern portfolio allocations navigated the COVID-19 crisis well and are positioned to take advantage of whatever market storms are on the horizon.

Other possible reasons for investing in alternatives

Forbes published a short article detailing five possible reasons why investing in alternatives is taking off. The reasons are as follows:

- Many investors are tired of hair-raising volatility.

- Equities remain expensive, and forecasted future returns look less appealing.

- Low interest rates are depressing returns.

- Investors are planning for higher inflation.

- Technology is democratizing alternative investments.

We covered number 1 in our piece Arbitraging Liquidity: Understanding the Liquidity Premium and while this is an enticing feature of investing in alternatives, it is not a main driver; it is an added incentive that would not be tolerated if returns were not generated.

Reasons 2 and 3 are seen by many investors as really boiling down to the same risk. Low rates are depressing current returns on bonds, but corporations have accessed cheap rates to lower their cost of capital and increase their valuations. We agree.

Reason 4, investors planning for inflation may certainly drive a decision towards investing in alternatives. While we have covered the issue before, it should be added that pension funds often do not need to worry about inflation, and in fact could be large beneficiaries of inflation because it would lower their obligations in real terms. So, while inflation fears should influence individuals’ investment behavior, institutions may actually benefit from it.

Reason 5 is in its most nascent stages, and it is where partners like Crystal seek to play a role for financial advisors.

How Do Pension Plans Work?

The Tax Foundation states, “Pension plan structures vary from state to state, but historically, most states have provided some form of defined benefit plan that promises retirees a lifetime annuity.”

Said more simply, pensioners can expect to receive fixed periodic payments to fund their retirements. This means that pension schemes have long-term liabilities that they owe to past and current employees.

The key word here is LIABILITY.

The Tax Foundation continues:

In recent years, some states have transitioned to a defined contribution plan for new employees, with employees controlling their own accounts and employer contributions funded by the state. Other states have shifted to a hybrid plan that combines elements of a defined benefit and a defined contribution plan. The shift from defined benefit plans toward more fiscally responsible alternatives can help states better manage future liability, but many states still face years of underfunded obligations that will need to be fulfilled. (Tax Foundation, April 2020)

The words to key in on here are defined contribution versus defined benefit in the preceding quote.

Defined contributions are more fiscally responsible because once an employer submits this piece, their financial obligation is over. The employer may still be obligated to act as a fiduciary, but they do not have a return hurdle that they are required to meet.

The core point is defined benefits result in future liabilities.

Because each state has liabilities that they owe, they take stock of the assets that they contributed versus what they owe to pensioners. The Pension Plans also calculate a return that is achievable and lessens the amount they must contribute.

Pension Funds Expect Lower Returns Going Forward

The Pew Charitable Trust writes, “The present value of future liabilities is typically calculated using the assumed rate of return as the discount rate, which is used to express future liabilities in today’s dollars; lower return assumptions yield higher calculated liabilities.”

And the following chart from Pew shows that pension plans are lowering their expected returns. This is reasonable given the decline in interest rates.

Public Pension Fund Median Assumed Rate of Return

Plans lower return targets in anticipation of continued low economic growth

Source: State Comprehensive Annual Financial Reports; state treasury reports; quarterly investment reports; and state responses to data inquiries

© 2019 The Pew Charitable Trusts

Pew’s database is comprehensive on this subject:

Pew’s database includes the 73 largest state-sponsored pension funds, which collectively manage 95 percent of all investments for state retirement systems. The average assumed return for these funds was 7.3 percent in 2017, down from over 7.5 percent in 2016 and 8 percent in 2007 just before the downturn began.

Investing in Alternatives May Help Solve a Lurking Problem

One glaring issue not yet mentioned here is that numerous pension plans are relatively underfunded today.

Assets and Liabilities of State Pension Plans Over Time

Widening gap between assets and liabilities mean financial challenges ahead for some states

Source: The Pew Charitable Trusts. November 2020. “State Retirement Fiscal Health and Funding Discipline.”

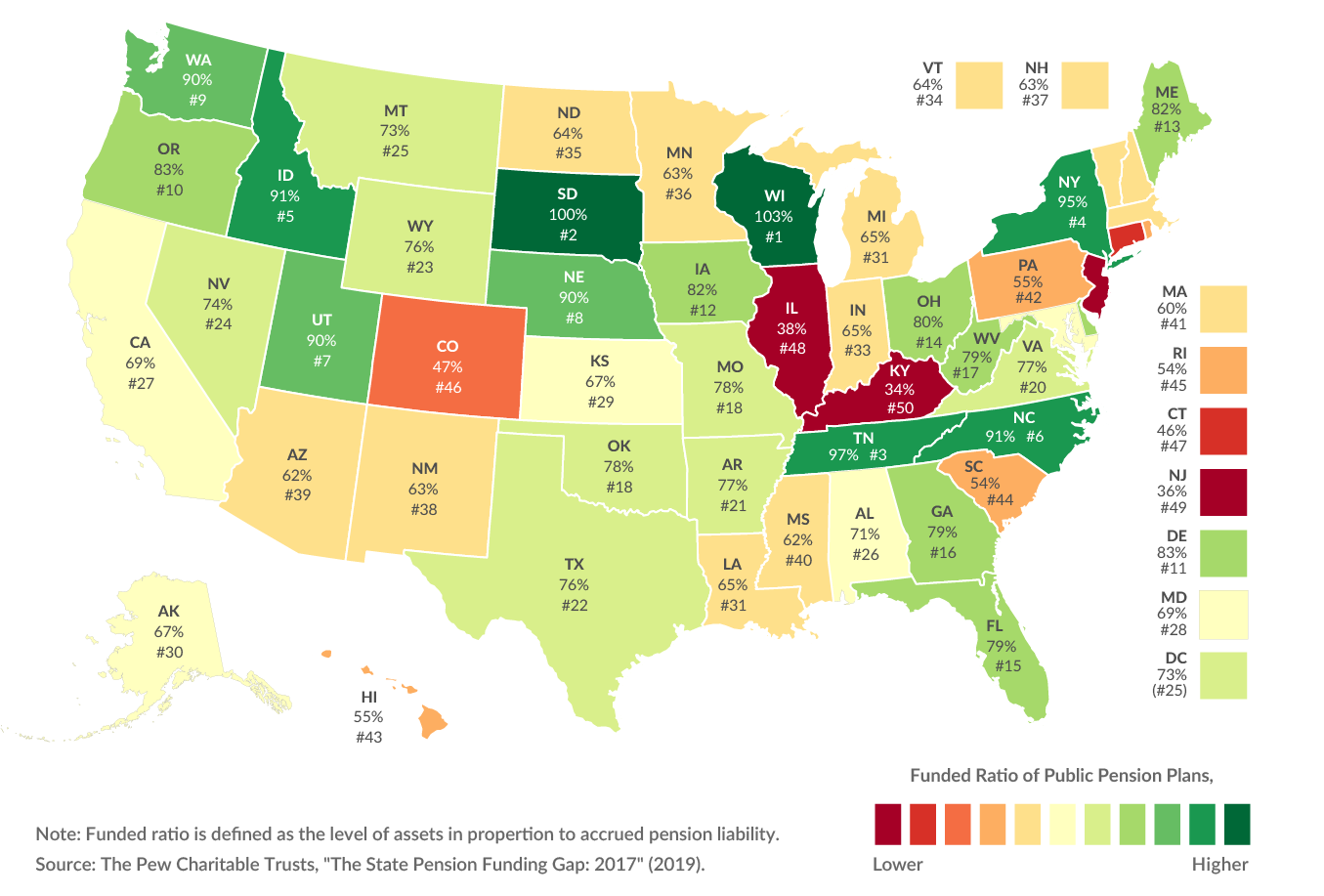

How Well-Funded are Pension Plans in Your State?

Funded Ratio of Public Pension Plans, Fiscal Year 2017

According to the Tax Foundation’s map, only two funds are fully funded and, although a handful of others are mighty close, many more are at risk of needing to increase contributions in order to achieve their defined benefit goals. Increasing the amount of money that states contribute to their pension plans could put a strain on state budgets when many are in the process of cutting services to make their budgets balance as a result of the COVID-19 pandemic and other factors.

Conclusion

Investing in alternatives is gaining popularity. The two main drivers in the continued growth in alternatives are low interest rates and the need for some pension funds to hit return thresholds that have not gone down nearly as much interest rates have.

As pension funds drive investment flows towards alternatives in order to achieve their investment goals, they could very well cause a reinforcing cycle of pushing up the valuations of alternatives.

Individual investors have much lower allocations to alternatives. Investing in alternatives may help individuals avoid lowering their return thresholds. If financial advisors follow the endowment model for their clients’ portfolios, then the benefits of increased allocations to alternatives can flow through to them.

Gain exposure to institutional private equity and hedge fund strategies that may minimize risk for your clients' portfolios.

For financial professionals only.